Curve fit models

There are several different models available for curve fitting. The various models are briefly explained here.

See also Lines and curves.

Straight line

where a is the intercept and b is the slope.

Logarithmic

where

a and

b are constants and

ln is the natural logarithm function. This model requires that

x>0 for all data points. Spotfire uses a nonlinear

regression method for this calculation. This will result in better accuracy of

the calculation compared to using linear regression on transformed values only.

Exponential

where a and b are constants, and e is the base of the natural logarithm.

Exponential models are commonly used in biological applications, for example, for exponential growth of bacteria. Spotfire uses a nonlinear regression method for this calculation. This will result in better accuracy of the calculation compared to using linear regression on transformed values only.

Power

where a and b are constants. This model requires that x>0 for all data points, and either that all y>0 or all y<0. Spotfire uses a nonlinear regression method for this calculation. This will result in better accuracy of the calculation compared to using linear regression on transformed values only.

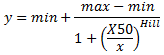

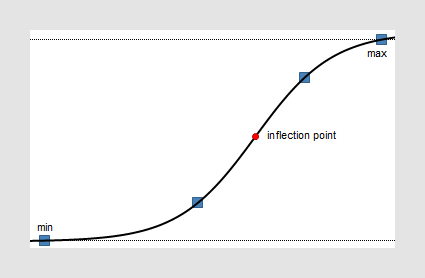

Logistic regression

The logistic regression fit is a dose response ("IC50") model, also known as sigmoidal dose response. The four parameter logistic model is the most important one.

Dose-response curves describe the relationship between response to drug treatment and drug dose or concentration. These types of curves are often semi-logarithmic, with log (drug concentration) on the X-axis. On the Y-axis, you can show measurements of enzyme activity, accumulation of an intracellular second messenger or measurements of heart rate or muscle contraction.

Log10-transformed X-values

The LoggedX50 value is interpreted as the Log10(X50). For example, if the H30+ concentration at IC50 has a pH of 3, then the LoggedX50 = -3.

Non-logarithmic X-values

x>0 for all data points and that you use at least

four records to calculate the curve.

Polynomial

where a0, a1, a2, etc., are constants. The default order is a 2nd order polynomial, but you can change the degree in the settings for the curve. This model requires that you use at least three markers to calculate the curve for a 2nd order polynomial model, and four markers for a 3rd order polynomial, and so on.

If you have a low number of unique x-values, a polynomial curve can be calculated in an unlimited number of ways. This means that you might end up with a curve that does not look as expected. If this happens, you probably should not apply this model to your data.

Some of the models have been partially solved by using the LAPACK software package, see References.

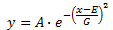

Gaussian

where A is the amplitude (height) of the curve, E is the position of the center of the curve and G is the width.

In Spotfire, you have the possibility to let the application calculate values on the parameters A, E and G automatically from the available data by leaving the curve parameter fields blank. You can also specify one or more of the parameters yourself.

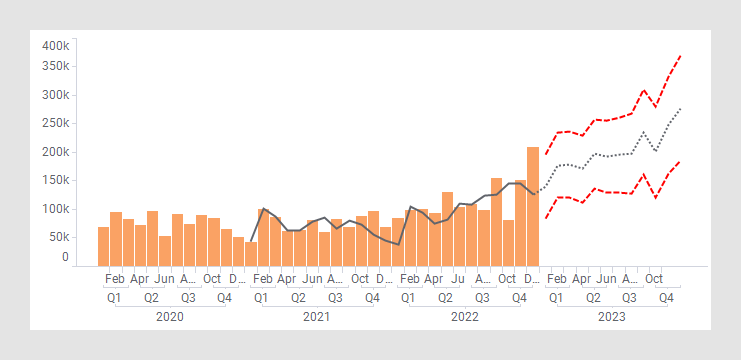

Holt-Winters forecast

The Holt-Winters Forecast uses Spotfire® Enterprise Runtime for R (a/k/a TERR™) to compute the Holt-Winters filtering of a time series or anything that can be coerced to a time series. This is an exponentially weighted moving average filter of the level, trend, and seasonal components of a time series. The smoothing parameters are chosen to minimize the sum of the squared one-step ahead prediction errors.

The output of a Holt-Winters Forecast is three different curves: a fitted curve showing the general variation of the measure of interest, a forecast curve predicting the future trend and a confidence interval showing how the insecurity increases the further away from the known values the prediction reaches.

- Level

(alpha) – Specifies how to smooth the level component of the time

series.

The level (alpha) parameter must be larger than 0 but not larger than 1.

A small value means that older values in the X direction are weighted more heavily.

Values near 1.0 mean that the latest value has more weight.

-

Trend (beta) – Specifies how to smooth the

trend component of the time series.

The trend (beta) parameter must be in the interval of 0-1.

A small value means that older values in X direction are weighted more heavily.

Values near 1.0 mean that the latest value has more weight.

- Seasonal

(gamma) – Specifies how to smooth the seasonal component of the

time series.

The seasonal (gamma) parameter must be in the interval of 0-1.

A small value means that older values in X direction are weighted more heavily.

Values near 1.0 mean that the latest value has more weight.

Use the drop-down list to specify how the seasonal component should interact with the other components:

Additive (default) indicates that X is modeled as level + trend + seasonal.

Multiplicative indicates the model is (level + trend) * seasonal.

-

Frequency – Only applicable when a Seasonal

(gamma) component is included in the model.

Specifies the number of seasonal periods to use to compute start values, that is, the number of observations per sampling period. For example, monthly data have a frequency of 12. The frequency must be greater than 1 to fit a seasonal component.

- Time points

ahead – Specifies the number of time points (nodes) into the future

at which to predict the values of the time series.

If the visualization shows months, then the time points ahead equals the number of months forward to predict. If the visualization shows years, then the time points ahead represents the number of years forward to predict.

- Confidence level – Specifies the confidence level. This should be a number larger than 0 but not larger than 1.

- Allow replacement of empty values – Allows you to replace empty values by interpolating the adjacent values. Note that two missing data points in a row cannot be interpolated.

You can specify a frequency or the time points ahead, either using a fixed number or by using a property value, selected using the Set from Property functionality. The property value can in turn be changed by adding a property control in a text area. See Using document, data table or column properties in the analysis and the following topics for more information about properties and property controls.

The used parameters can be shown in labels or tooltips.